Discover and read the best of Twitter Threads about #Q3investorpresentations

Most recents (14)

#subex #Q3marketupdates #Q3concall #Q3updates

Concall transcript Q3fy21

Rev 93.9 cr ,Ebidta 20.3 cr & PAT 8.5 cr

9mfy21 Rev 275.9 cr up 6% yoy

Interim dividend of 10%

Moved into new corporate office in Bengaluru

In IoT focus on mftng sector,secured 4 new customers in Q3

Concall transcript Q3fy21

Rev 93.9 cr ,Ebidta 20.3 cr & PAT 8.5 cr

9mfy21 Rev 275.9 cr up 6% yoy

Interim dividend of 10%

Moved into new corporate office in Bengaluru

In IoT focus on mftng sector,secured 4 new customers in Q3

ID central (identity analytics solution) launched in Indonesia, 1st customer onboard

NGP platform, next gen platform to revolutionize way telcos operate in OSS & BSS system ,cloud native API based application

Expect more 5g contracts in APAC & ME in coming quarters

NGP platform, next gen platform to revolutionize way telcos operate in OSS & BSS system ,cloud native API based application

Expect more 5g contracts in APAC & ME in coming quarters

Vision to emerge as a leader in digital trust solutions in multi vertical environment

Closed about $28.5mn deals in 9mfy21 ,Q4 to exceed Q3 in deal wins

Tech mahindra partnership around Block chain area

New product offering for Telcos- Augmented Analytics platform

Closed about $28.5mn deals in 9mfy21 ,Q4 to exceed Q3 in deal wins

Tech mahindra partnership around Block chain area

New product offering for Telcos- Augmented Analytics platform

#galaxysurfactants #Q3investorpresentations

:Q2 momentum spilled into Q3

:Speciality segment double digit growth

:Domestic mkt double digit growth

:Interim dividend Rs 14

Vols Q3fy21/20

Performance surfactants 36618/34978

Speciality 21620/19295

Total 58238/54273

:Q2 momentum spilled into Q3

:Speciality segment double digit growth

:Domestic mkt double digit growth

:Interim dividend Rs 14

Vols Q3fy21/20

Performance surfactants 36618/34978

Speciality 21620/19295

Total 58238/54273

Revenue HLs

Q3fy21/20 in crs

Performance surfactants 401/387

Speciality 277/242

Total 678/629

PAT 85/48

9mnths fy21 vols

India mkt up 13.3%

Africa & ME Up 6.3%

ROW down -10.1%

9mnth FHs in cr

PS 1292/1187

Speciality 717/759

Total 2009/1946

PAT 223/168

Q3fy21/20 in crs

Performance surfactants 401/387

Speciality 277/242

Total 678/629

PAT 85/48

9mnths fy21 vols

India mkt up 13.3%

Africa & ME Up 6.3%

ROW down -10.1%

9mnth FHs in cr

PS 1292/1187

Speciality 717/759

Total 2009/1946

PAT 223/168

Truly Indian MNC

:Leading mftr of ingredients for home & personal care industry

:preferred supplier for MNC,Regional & local Fmcg

:205+ product grades

: 7 strategic facilities (5 India,1Egypt ,1 US)

: Extensive R&D capacity

: intellectual property- 78 approved,1e applied

:Leading mftr of ingredients for home & personal care industry

:preferred supplier for MNC,Regional & local Fmcg

:205+ product grades

: 7 strategic facilities (5 India,1Egypt ,1 US)

: Extensive R&D capacity

: intellectual property- 78 approved,1e applied

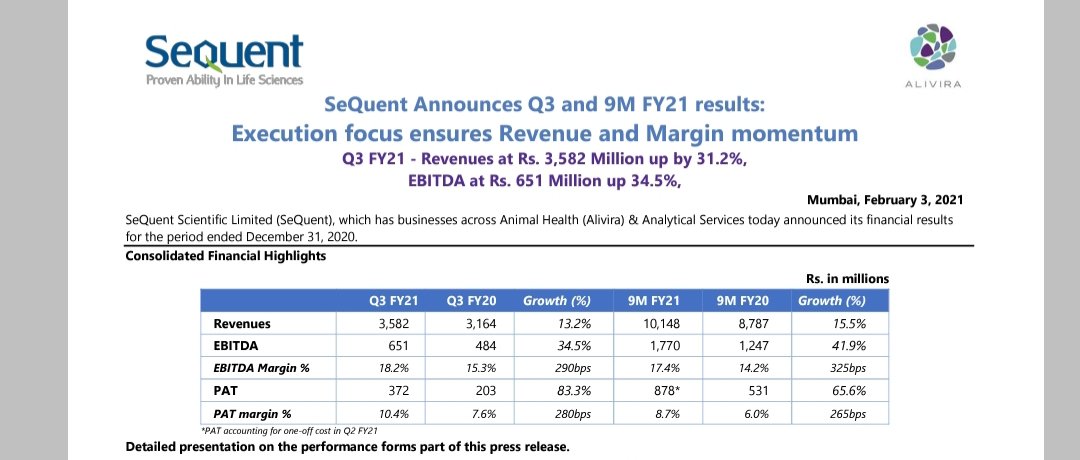

#sequentScientific #Q3marketupdates #Q3investorpresentations

Strong 🏋️♀️

Q3fy21/20 in cr

Rev 361/317

PAT 37.2/20

EPS 1.52/0.83

9mnth fy21/20

Rev 1014/878

PAT 87.8 /53.1

EPS 3.24/2.18

API Business up 17.2%

Formulations 15.0%

Alivira award best Company in AH India/ME/Africa

Strong 🏋️♀️

Q3fy21/20 in cr

Rev 361/317

PAT 37.2/20

EPS 1.52/0.83

9mnth fy21/20

Rev 1014/878

PAT 87.8 /53.1

EPS 3.24/2.18

API Business up 17.2%

Formulations 15.0%

Alivira award best Company in AH India/ME/Africa

Formulations

EU subdued due operational challenges of Covid

Spain & Germany impacted while Benelux & Sweden reported strong growth

Growth to accelerate with recent launches of CitramoxLA & Halofusol. Tulathromycin launch to reflect from the current quarter

EU subdued due operational challenges of Covid

Spain & Germany impacted while Benelux & Sweden reported strong growth

Growth to accelerate with recent launches of CitramoxLA & Halofusol. Tulathromycin launch to reflect from the current quarter

Brazil & Turkey grow strongly driven by mkt share gain existing portfolio & new launches

India business doubled last 9 months

Integration Zoetis portfolio completed

API Business

Highest quarterly sales 1,297Mn, growth 20%

1/3rd sales from global Top-10 AH players in 9M

India business doubled last 9 months

Integration Zoetis portfolio completed

API Business

Highest quarterly sales 1,297Mn, growth 20%

1/3rd sales from global Top-10 AH players in 9M

#solaraactivepharma

#Q3marketupdates #Q3investorpresentations

Best Ever Quarterly Revenue, EBITDA & PAT

Rev 4,350 mn, up 24% yoy & 8% qoq Q3’21 EBITDA 1,085 Mn, up 32% yoy & 8% qoq

PAT 658 Mn, up 59% yoy & 16% qoq

Basic EPS 18.47

#Q3marketupdates #Q3investorpresentations

Best Ever Quarterly Revenue, EBITDA & PAT

Rev 4,350 mn, up 24% yoy & 8% qoq Q3’21 EBITDA 1,085 Mn, up 32% yoy & 8% qoq

PAT 658 Mn, up 59% yoy & 16% qoq

Basic EPS 18.47

API Business

Regulated mkt rev 3110 mn, up 12% yoy

,contributed 72% of Q3’21 rev, decline from Q2 result of robust growth in other mkts

Other mkts rev 1240 mn, up 71% yoy

Rev growth 24% yoy (37% yoy ex-ranitidine) driven by growth in vol, scale up Vizag

New products 9% Q3’21rev

Regulated mkt rev 3110 mn, up 12% yoy

,contributed 72% of Q3’21 rev, decline from Q2 result of robust growth in other mkts

Other mkts rev 1240 mn, up 71% yoy

Rev growth 24% yoy (37% yoy ex-ranitidine) driven by growth in vol, scale up Vizag

New products 9% Q3’21rev

CRAMS

Tracking well to plan ,addition of new customers, solid growth order book

R&D & Ops

Vizag onstream, commercialized as planned in Q3

Filed 3 new DMFs US mkt ,2 EU mkt during Q3’21

Market extensions 6 of existing products across 7 different geographies

R&D 138 mn 3.2% Rev

Tracking well to plan ,addition of new customers, solid growth order book

R&D & Ops

Vizag onstream, commercialized as planned in Q3

Filed 3 new DMFs US mkt ,2 EU mkt during Q3’21

Market extensions 6 of existing products across 7 different geographies

R&D 138 mn 3.2% Rev

#subex #Q3marketupdates #Q3investorpresentations

9mnths fy21

Revenue up 6% ,2758 mn

Ebidta margin 27.3% ,753 mn

PAT (exc exp items) up 101% ,332.5 mn

Products :

Revenue assurance

IOT security

Fraud manag

Identity analytics

Anomaly detection

Network analytics

9mnths fy21

Revenue up 6% ,2758 mn

Ebidta margin 27.3% ,753 mn

PAT (exc exp items) up 101% ,332.5 mn

Products :

Revenue assurance

IOT security

Fraud manag

Identity analytics

Anomaly detection

Network analytics

3 horizon strategy

1 - enhance core areas ( fraud mang,Rev assurance ,Network analytics, partner ecosystem mang)

2 - immediate growth ( IOT security, Analytics center of trust)

3 - long term growth , invest in emerging areas ( Multi-Vertical SaaS)

Crunch metric

IDcentral

1 - enhance core areas ( fraud mang,Rev assurance ,Network analytics, partner ecosystem mang)

2 - immediate growth ( IOT security, Analytics center of trust)

3 - long term growth , invest in emerging areas ( Multi-Vertical SaaS)

Crunch metric

IDcentral

Investment rationale

Leader in Digital Trust space

Making strong inroads in the multi vertical IoT Security space; IoT Security Market to touch $4.5 bn by 2022

Incubating virtual startups within the orgztn

Sticky Revenue Model ,60% annuity/ recurring, >98% customer retentn

Leader in Digital Trust space

Making strong inroads in the multi vertical IoT Security space; IoT Security Market to touch $4.5 bn by 2022

Incubating virtual startups within the orgztn

Sticky Revenue Model ,60% annuity/ recurring, >98% customer retentn

#emamiltd #Q3marketupdates #Q3investorpresentations

Concall highlights

Rural demand remained strong, urban showed pickup

Healthcare portfolio showed good response due to covid

Product penetration of 4% for Boroplus,Balms,Kesh king,etc

Double digit vol growth guidance for Q4

Concall highlights

Rural demand remained strong, urban showed pickup

Healthcare portfolio showed good response due to covid

Product penetration of 4% for Boroplus,Balms,Kesh king,etc

Double digit vol growth guidance for Q4

Manag confident of new launches Boroplus,Emasol

Honey controversy appears to settle down, mkt changing from seasonal to perennial

Fair & Handsome sales showing uptick post rebranding, relaunch

Sanitiser sales witnessing slowdown

Hair oils seeing demand in domestic & ME mkts

Honey controversy appears to settle down, mkt changing from seasonal to perennial

Fair & Handsome sales showing uptick post rebranding, relaunch

Sanitiser sales witnessing slowdown

Hair oils seeing demand in domestic & ME mkts

Q3 sales Zandu segment

Honey up 2.5% ,Chyawanprash 24%

International business up 26% yoy led by growth in ME & SAARC ,new launches contributed 4% to sales in Q3 ,creme21 grew 82%

30+ new product launches Fy21

E comm sales up 3.5x in Q3 ,up 210 bps

MT channel growth 51% in Q3

Honey up 2.5% ,Chyawanprash 24%

International business up 26% yoy led by growth in ME & SAARC ,new launches contributed 4% to sales in Q3 ,creme21 grew 82%

30+ new product launches Fy21

E comm sales up 3.5x in Q3 ,up 210 bps

MT channel growth 51% in Q3

@LaurusLabs #lauruslabs #Q3marketupdates #Q3investorpresentations

Q3fy21/20 in crs

Rev 1288/730 ,up 76%

Ebidta 433/150

PAT 273/73 ,up 274%

EPS 5.1/1.4

Generic API growth 103% yoy

ARVs up 175% yoy

Generic FDF up 47%

Custom synthesis up 63% yoy

Onco API growth 36%

Q3fy21/20 in crs

Rev 1288/730 ,up 76%

Ebidta 433/150

PAT 273/73 ,up 274%

EPS 5.1/1.4

Generic API growth 103% yoy

ARVs up 175% yoy

Generic FDF up 47%

Custom synthesis up 63% yoy

Onco API growth 36%

Generic APIs

ARV,Anti-DM,CVS,PPIs,Onco

Commercialized 60+ products

61 DMFs filed

Generic FDF

ARV,Anti-DM,CVS,PPIs,Onco

Filed 26 ANDAs with USFDA

9 final & 8 tentative approvals

Filed 12 dossiers in Canada, 9 in EU ,8 with WHO,2 in S.Africa, 2 in India

ARV,Anti-DM,CVS,PPIs,Onco

Commercialized 60+ products

61 DMFs filed

Generic FDF

ARV,Anti-DM,CVS,PPIs,Onco

Filed 26 ANDAs with USFDA

9 final & 8 tentative approvals

Filed 12 dossiers in Canada, 9 in EU ,8 with WHO,2 in S.Africa, 2 in India

Laurus Synthesis

CDMO services for Global pharma

Steroids,hormone mftg

Speciality ingredients in Nutraceuticals,dietary,cosmetics

Commercial scale mfg,clinical phase supplies,Analytics & research

API validation plannd in Unit 5

Optalmic initiated

LSPL-API validatn planned

CDMO services for Global pharma

Steroids,hormone mftg

Speciality ingredients in Nutraceuticals,dietary,cosmetics

Commercial scale mfg,clinical phase supplies,Analytics & research

API validation plannd in Unit 5

Optalmic initiated

LSPL-API validatn planned

@GranulesIndia #granulesindia #Q3marketupdates #Q3investorpresentations

Q3Fy21 Highlights Revenue from ops up 20% yoy driven by 4 new launches in Q3 & increase in mkt share existing products across the three segments – API, PFI and FD

Q3Fy21 Highlights Revenue from ops up 20% yoy driven by 4 new launches in Q3 & increase in mkt share existing products across the three segments – API, PFI and FD

EBITDA up 29.7% yoy, +190 bps margin expansion yoy on changing product mix with higher contribution from FD and PFI , improved operational efficiencies from higher capacity utilization

PAT 147 cr up 129.4% yoy

Net Debt down 22% yoy

Net debt to EBITDA 0.7x vs. 1.4x as of Q3fy20

PAT 147 cr up 129.4% yoy

Net Debt down 22% yoy

Net debt to EBITDA 0.7x vs. 1.4x as of Q3fy20

ROCE 32.4%, up on account of higher capacity utilization via addition of new modules & equipment with limited capital expenditure

Q3fy21 launched Ramelteon, Dexmethylphenidate HCI and Potassium Chloride ER tablets (Klor-Con), from GPI and Guaifenesin ER tablets from GIL

Q3fy21 launched Ramelteon, Dexmethylphenidate HCI and Potassium Chloride ER tablets (Klor-Con), from GPI and Guaifenesin ER tablets from GIL

@ApolloTriCoat

#Q3marketupdates #Q3investorpresentations

Apollo tricoat - 3 steps ahead

Q3fy21/20 in crs

Rev 503/229

PAT 38/18

EPS 12.46/5.93

9m fy21/20

Rev 1006/434

PAT 70/31

EPS 23.24/10.35

Full on ahead not only 3 steps

#Q3marketupdates #Q3investorpresentations

Apollo tricoat - 3 steps ahead

Q3fy21/20 in crs

Rev 503/229

PAT 38/18

EPS 12.46/5.93

9m fy21/20

Rev 1006/434

PAT 70/31

EPS 23.24/10.35

Full on ahead not only 3 steps

50 % mkt share in structural steel tubes 9mfy21,sales vol CAGR 27% fy11-20

Most products with 1500+ SKUs (shapes & sizes)

Highest scale with 10 plants - 2.5 mn ton capacity

Largest sales network 800+ distributors

Lowest cost producer

Premium pricing to peers

50000+ retailers

Most products with 1500+ SKUs (shapes & sizes)

Highest scale with 10 plants - 2.5 mn ton capacity

Largest sales network 800+ distributors

Lowest cost producer

Premium pricing to peers

50000+ retailers

Existing product portfolio

Door solution - Chaukhat (Indias 1st closed steel door frame ) ,monthly sales reached 4000 ton ,2 lakh/month chaukhats ,UP,HP,Rajsthn,Punjab

Home beautification - Elegant ,Signature, Plank

Door solution - Chaukhat (Indias 1st closed steel door frame ) ,monthly sales reached 4000 ton ,2 lakh/month chaukhats ,UP,HP,Rajsthn,Punjab

Home beautification - Elegant ,Signature, Plank

@PolycabIndia #Q3marketupdates #Q3investorpresentations

Q3 earnings presentation

Revenue Q3 27988 mn ,up 12% yoy

9m 58891 mn ,up 12% yoy

PAT 2636mn ,up 19% yoy

9m 6027 mn,up 9% yoy

Net cash Q3 - 1335 mn

Q3 earnings presentation

Revenue Q3 27988 mn ,up 12% yoy

9m 58891 mn ,up 12% yoy

PAT 2636mn ,up 19% yoy

9m 6027 mn,up 9% yoy

Net cash Q3 - 1335 mn

Wires&cables

6% yoy growth

Distribution channel double digit growth

Institutional businesses continues 2 face headwinds

Wires > cables

Housing wires strong momentum

Export 2.9 bn,10.5% overall sales,down 33% yoy due higher Dangote base

Exc Dangote, Aus,Asia,UK 29% yoy growth

6% yoy growth

Distribution channel double digit growth

Institutional businesses continues 2 face headwinds

Wires > cables

Housing wires strong momentum

Export 2.9 bn,10.5% overall sales,down 33% yoy due higher Dangote base

Exc Dangote, Aus,Asia,UK 29% yoy growth

Fast moving electrical goods

Strong 41% yoy growth in total Rev back of consumer demand,distribution, product mix

FMEG mix to sales up 215bps, up 10.8% yoy

Fans took leadership in few geographies

Segment Ebit margin 5.9% in Q3 & 4.7% in 9mnths

Strong 41% yoy growth in total Rev back of consumer demand,distribution, product mix

FMEG mix to sales up 215bps, up 10.8% yoy

Fans took leadership in few geographies

Segment Ebit margin 5.9% in Q3 & 4.7% in 9mnths

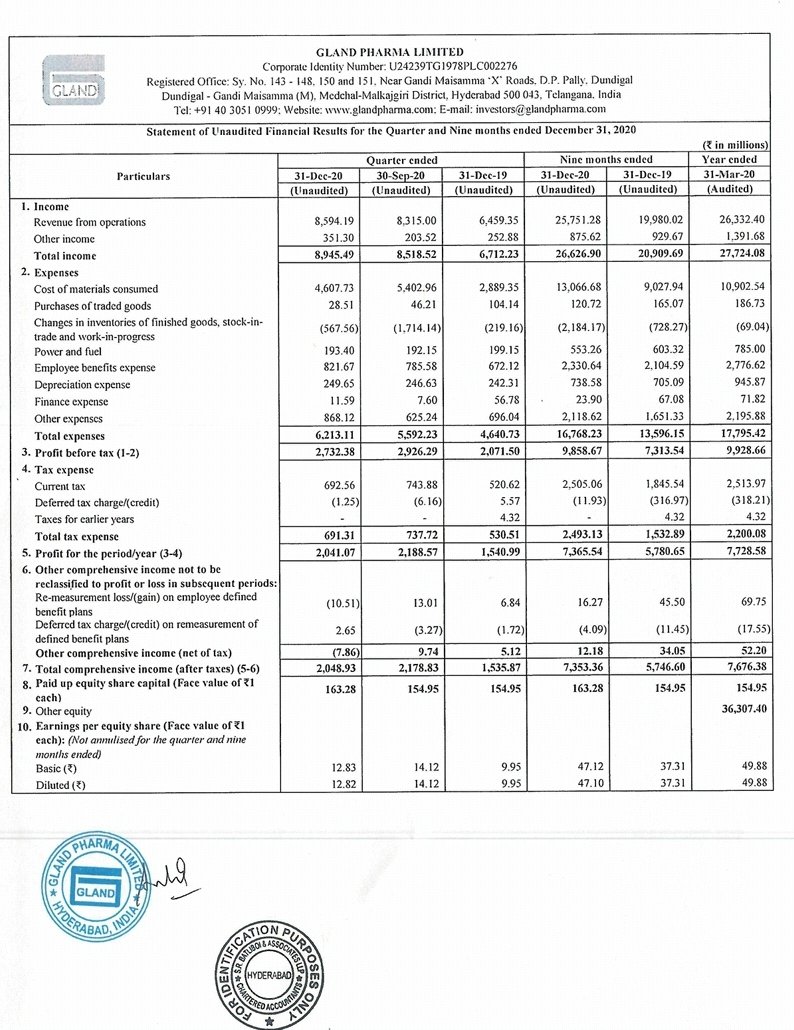

#glandpharma

#Q3marketupdates #Q3investorpresentations

Good show inr in mn

Rev 8945 /6712

PAT 2041 /1540

EPS 12.83 /9.95

9 months fy21 /20

Rev 26626 /20909

PAT 7365 /5780

EPS 47.12 / 37.31

Mkt wise

US 6021 /4853

India 1495 /1193

ROW 1078/413

#Q3marketupdates #Q3investorpresentations

Good show inr in mn

Rev 8945 /6712

PAT 2041 /1540

EPS 12.83 /9.95

9 months fy21 /20

Rev 26626 /20909

PAT 7365 /5780

EPS 47.12 / 37.31

Mkt wise

US 6021 /4853

India 1495 /1193

ROW 1078/413

R&D expenses INR Mn

Q3 fy21 434

Q3fy20 312

9M Fy21 916

9m Fy20 749

Net worth INR Mn

Mar 20 36462

Dec 20 56221

Net cash INR Mn

Mar 20 13202

Dec 20 28128

Capital expenditure

9M Fy20 1342

9M Fy21 1826

CFO

9M Fy20 4244

9M fy21 4056

Q3 fy21 434

Q3fy20 312

9M Fy21 916

9m Fy20 749

Net worth INR Mn

Mar 20 36462

Dec 20 56221

Net cash INR Mn

Mar 20 13202

Dec 20 28128

Capital expenditure

9M Fy20 1342

9M Fy21 1826

CFO

9M Fy20 4244

9M fy21 4056

New launches

9months fy21 - 31 product SKUs (4 mols)

US mkt - Dec 20 ,with partners filed 282 ANDAs, 226 approved, 56 pending

Core mkts (US,EU,Canada,Australia)

9M fy21 17415 mn

Growth 20%

Q3 fy21 6021 mn

Growth 24%

Domestic MKT

9M fy2110 product SKUs

Started Remdesivir mftg

9months fy21 - 31 product SKUs (4 mols)

US mkt - Dec 20 ,with partners filed 282 ANDAs, 226 approved, 56 pending

Core mkts (US,EU,Canada,Australia)

9M fy21 17415 mn

Growth 20%

Q3 fy21 6021 mn

Growth 24%

Domestic MKT

9M fy2110 product SKUs

Started Remdesivir mftg

@HDFCLIFE #Q3marketupdates #Q3investorpresentations

Mkt share up 214 bps to 16.4%

NBM at 25.6%

8% Individual WRP growth compared to private industry de-growth of 6%

25.6% New Business Margin on the back of growth, balanced product mix

Mkt share up 214 bps to 16.4%

NBM at 25.6%

8% Individual WRP growth compared to private industry de-growth of 6%

25.6% New Business Margin on the back of growth, balanced product mix

17% growth in Protection (Indl) and 42% growth in Annuity in APE terms

22% growth in renewal premium with stable persistency

PAT of Rs 1,042 Cr, with growth of 6%

Solvency healthy at 202%

22% growth in renewal premium with stable persistency

PAT of Rs 1,042 Cr, with growth of 6%

Solvency healthy at 202%

Pvt mkt share rank up to 2,gain 214 bps 14.3 to 16.4%

Balanced product mix %

Savings 35

Non participating savings 30

Ulips 23

Protection 7

Annuity 5

Distribution 300+ partners

AUM 31Dec 20

1.7 lkh cr

Debt:equity mix 64:36

98% debt in Gsecs & AAA

Renewal premium growth 22%

Balanced product mix %

Savings 35

Non participating savings 30

Ulips 23

Protection 7

Annuity 5

Distribution 300+ partners

AUM 31Dec 20

1.7 lkh cr

Debt:equity mix 64:36

98% debt in Gsecs & AAA

Renewal premium growth 22%

@SyngeneIntl #Syngene #Q3marketupdates

Q3fy21/20 in mn

Rev 5845 /5191

Ebidta 1933 /1735

PAT 1022 /918

9months fy21 /20

Rev 15257/14046

Ebidta 5026/4749

PAT 2443 /2460

Q3fy20 had exceptional gain of 459 mn leading to higher PAT

Good show

High conviction bet

Doubler for me

Q3fy21/20 in mn

Rev 5845 /5191

Ebidta 1933 /1735

PAT 1022 /918

9months fy21 /20

Rev 15257/14046

Ebidta 5026/4749

PAT 2443 /2460

Q3fy20 had exceptional gain of 459 mn leading to higher PAT

Good show

High conviction bet

Doubler for me

#Q3investorpresentations

Collaborated Deerfield discovery & development 3DC to advance integrated drug discovery projects, early target validation to preclinical evaluation

Expanded research facility Genome valley Hyderabad, +90 scientist

Accreditatn NABL fr medical devices

Collaborated Deerfield discovery & development 3DC to advance integrated drug discovery projects, early target validation to preclinical evaluation

Expanded research facility Genome valley Hyderabad, +90 scientist

Accreditatn NABL fr medical devices

Setup new RT-PCR testing facility approved by NABL & ICMR

360clients

20395 mn Rev Fy20

8 Collaborations with top 10 pharma companies

4200 + scientists

3662 mn PAT fy20

400+ patents ( held with clients )

31541 mn capex Mar 20

Integrated services- drug discovery,development,mfg

360clients

20395 mn Rev Fy20

8 Collaborations with top 10 pharma companies

4200 + scientists

3662 mn PAT fy20

400+ patents ( held with clients )

31541 mn capex Mar 20

Integrated services- drug discovery,development,mfg

@ICICILombard

Q3 & 9 months investor presentation

Leading pvt non life insurer since 2004

12 yr GDPI CAGR 12.3%

Mkt share 9 mns 7.2%

Agents 55615

Increasing share tier 3,4 cities

Virtual offices 840

Solvency Dec 20 - 2.76x ( req1.5x)

#Q3marketupdates

#Q3investorpresentations

Q3 & 9 months investor presentation

Leading pvt non life insurer since 2004

12 yr GDPI CAGR 12.3%

Mkt share 9 mns 7.2%

Agents 55615

Increasing share tier 3,4 cities

Virtual offices 840

Solvency Dec 20 - 2.76x ( req1.5x)

#Q3marketupdates

#Q3investorpresentations

In rs billion 9 mfy20 /21

Gross written premium 103.6 / 107.6

GDPI 101.32 /105.25

PAT 9.12 /11.27

ROE 21.8 /22.4%

Solvency ratio 2.18 /2.76x

BV 128.76/159.86

EPS 20.07/24.81

Product mix in %

Motor OD & TP 50/49

Motor GDPI Mix

Pvt car 55.9/57.4

2 wheeler 29.6/27.3

CV 14.5/15.3

Gross written premium 103.6 / 107.6

GDPI 101.32 /105.25

PAT 9.12 /11.27

ROE 21.8 /22.4%

Solvency ratio 2.18 /2.76x

BV 128.76/159.86

EPS 20.07/24.81

Product mix in %

Motor OD & TP 50/49

Motor GDPI Mix

Pvt car 55.9/57.4

2 wheeler 29.6/27.3

CV 14.5/15.3

Advanced premium Dec 31st 20 - 31.97 bn / Sep 20 - 31.6 bn

Health ,travel & PA GDPI Mix 9 mon fy20/21

Individual 22.5 /24.9%

Group others 40 /23.2%

Group employer-employee 37.4 /51.9

Individual health indemnity grew 25.7% for 9 month from 17 at Sep 20

Health ,travel & PA GDPI Mix 9 mon fy20/21

Individual 22.5 /24.9%

Group others 40 /23.2%

Group employer-employee 37.4 /51.9

Individual health indemnity grew 25.7% for 9 month from 17 at Sep 20