Its weekend...and time for deep dive for next #megatrend in the making ..

Can #textiles be the sector in 2022 what did speciality chemicals used to be in 2016-17??

Yes you are right speciality chemicals baskets have been 15-20 baggers in the last 5 years

(1/n)

Can #textiles be the sector in 2022 what did speciality chemicals used to be in 2016-17??

Yes you are right speciality chemicals baskets have been 15-20 baggers in the last 5 years

(1/n)

#Navinfluorine from 270 in 2016 to 4000 in 2021

#Vinatiorganics from 200 in 2016 to 2200 in 2021

#Aartiindustries from 135 in 2016 to 1200 in 2021

And lots many…

First of all, let us understand what’s exactly changed during 2016 for speciality

#Vinatiorganics from 200 in 2016 to 2200 in 2021

#Aartiindustries from 135 in 2016 to 1200 in 2021

And lots many…

First of all, let us understand what’s exactly changed during 2016 for speciality

chemicals and can history repeat itself in the case of textiles:

Flashback 2016:

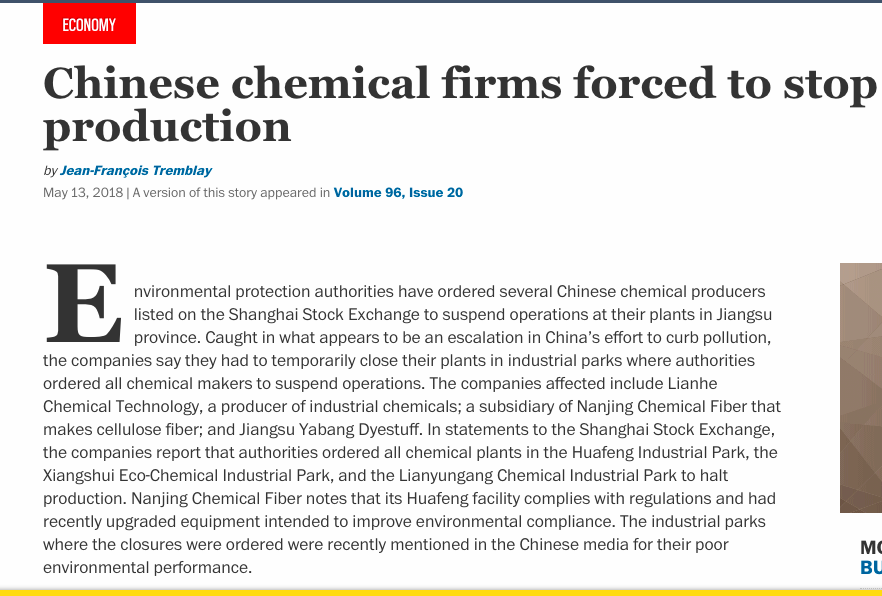

Back in 2016 china had a dominant market share of 67 % in speciality and commodity chemicals.

Due to rising Air pollution, Chinese regulations decided to shut down chemical factories

Flashback 2016:

Back in 2016 china had a dominant market share of 67 % in speciality and commodity chemicals.

Due to rising Air pollution, Chinese regulations decided to shut down chemical factories

Closure of Chinese chemicals factories induced supply-chain disruptions and thus the burden to substitute falls on Indian chemicals companies.

This change was structural in nature and was not going to fade away soon

This change was structural in nature and was not going to fade away soon

Indian companies witnessed a significant surge in revenue as well as operating margins

Sales of SRF almost doubled in 5 years with 100 basis pts increase in margins

Sales of SRF almost doubled in 5 years with 100 basis pts increase in margins

This entire chemical sector was up for re-rating since the growth in sales and sustainability in margins was visible

The chemical sector which traded @ 10-15 PE in 2016 is trading @50-70(Agree it’s a bit overvalued today)

PE earnings and EPS chart for SRF:

The chemical sector which traded @ 10-15 PE in 2016 is trading @50-70(Agree it’s a bit overvalued today)

PE earnings and EPS chart for SRF:

Now let’s come to the present for the Textile sector,

Over the years, China has maintained its dominance in textile and apparel (T&A) exports

However, this phenomenon is gradually changing as global manufacturers are moving away

Over the years, China has maintained its dominance in textile and apparel (T&A) exports

However, this phenomenon is gradually changing as global manufacturers are moving away

from China to diversify and shift manufacturing to other competing nations. China’s share in T&A exports dropped from 39% in 2015 📉 to 34 % In 2021

Now How India is in sweet spot and is well placed to cash in this opportunity:

1. CHINA + 1:

COVID-19-induced supply-chain disruptions and US-China trade tension have accelerated the pace at which companies are diversifying their base.

1. CHINA + 1:

COVID-19-induced supply-chain disruptions and US-China trade tension have accelerated the pace at which companies are diversifying their base.

2.Indian labour is 3x less expensive than China.

3.Indian cotton is 30% cheaper than Chinese cotton

4. India is one of the most cost-competitive textile manufacturing countries with a wide presence across the T&A value chain,

3.Indian cotton is 30% cheaper than Chinese cotton

4. India is one of the most cost-competitive textile manufacturing countries with a wide presence across the T&A value chain,

making it one of the strongest contenders of the Chinese dominance in the global T&A space.

4. Furthermore, the US has now banned imports made of Xinjiang cotton (Xinjiang region accounts for 20% of the global and ~85% of the Chinese cotton production).

4. Furthermore, the US has now banned imports made of Xinjiang cotton (Xinjiang region accounts for 20% of the global and ~85% of the Chinese cotton production).

Thus, the burden to substitute the cotton yarn used in these products falls on India (having the second-largest spindle capacity in the world). Due to this, the export demand for Indian yarn is on the rise with a resultant increase in domestic prices of yarn by nearly 80%

since Aug’20 (INR179/kg in Aug’20 vs INR318/kg in Nov’21)

5. To further cement India’s position in global textiles, the textile ministry under Mr Piyush Goyal is in conversation with multiple developed nations such as the UK, the EU, Canada and Australia over free trade agreements.

The UK and the EU are key apparel destinations for India. If FTAs are passed, India will be able to compete with garment powerhouses such as Bangladesh, China, Vietnam and Pakistan (Bangladesh, Vietnam and Pakistan currently enjoy free trade in most categories).

Even a marginal slip in the share of any of these countries in favour of India will lead to huge gains.

6. The government approved the continuation of the Rebate of State and Central Taxes and Levies (RoSCTL) scheme on exports of apparel, garments and made-ups until 2024.

6. The government approved the continuation of the Rebate of State and Central Taxes and Levies (RoSCTL) scheme on exports of apparel, garments and made-ups until 2024.

7. The initiative is inspired by the 5F vision of Prime Minister Modi. The '5F' Formula encompasses - Farm to fibre; fibre to factory; factory to fashion; fashion to foreign

8. Mega Integrated Textile Region and Apparel (PM MITRA) Parks to bring supply-chain and logistics cost down aiding better margins and Also not only will boost the competitiveness of the textile sector globally but also greatly enhance the profitability of textile companies.

Owing to the above tailwinds in the textile sector, history is just repeating itself, In 2017 it was chemicals and in 2021 its textiles.

The entire Textile sector is up for PE re-rating

The entire Textile sector is up for PE re-rating

Currently, we see margins surge from 15-16 % to 22-24 % (sales yet to pick up though)

All textiles companies except KPR and Gokaldas exports trade below PRICE/EARNINGS of 15 (most of them trade below 10)

P&L for KPR and filatex india

All textiles companies except KPR and Gokaldas exports trade below PRICE/EARNINGS of 15 (most of them trade below 10)

P&L for KPR and filatex india

Sales and margin improvement for KPR mills along with PE rerating chart for KPR MILLS.

Key Risks:

1.Delay in execution in government policies towards textiles sector

2.Contraction of cotton yarn spreads and Sustained supply chain issues to impact overall margins.

3. Managing huge labour force

1.Delay in execution in government policies towards textiles sector

2.Contraction of cotton yarn spreads and Sustained supply chain issues to impact overall margins.

3. Managing huge labour force

Stocks worth a look in Textiles sector :

#KPRmills

#sangamindia

#filatex

#gokaldas

#sutlej

#kitex

Disc: Biased and Invested from lower levels

Hit Likes and retweet for maximum reach to our investing community..Also gives us motivation to write and research more..

#KPRmills

#sangamindia

#filatex

#gokaldas

#sutlej

#kitex

Disc: Biased and Invested from lower levels

Hit Likes and retweet for maximum reach to our investing community..Also gives us motivation to write and research more..

• • •

Missing some Tweet in this thread? You can try to

force a refresh