Who’s up for a thread on the IRS Memo regarding daily fantasy sports contests and whether #DFS entry fees should be treated as “wagers” subject to a federal excise tax? Or should I save it for the next episode of @ConDetrimental? Either way, I’ll explain why the IRS got it wrong.

Thread on IRS Memo re: daily fantasy sports

The core issues are two-fold: (1) are DFS entry fees "wagers"? and (2) are DFS contest operators engaged in "the business of accepting wagers" through their acceptance of entry fees to compete in contests? The answer to both questions is "no" (IMO), and I will explain why below.

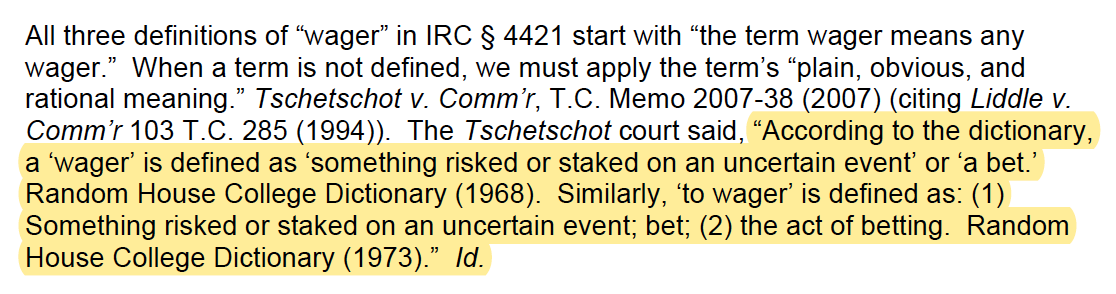

First, there is no independent definition of "wager" under the Internal Revenue Code. And to confuse matters, the Treasury Regs provide a completely meaningless circular definition of the word "wager," essentially defining a "wager" as a "wager." Essentially meaningless.

So, how, then, does the IRS attorney arrive at a definition of the word "wager"? She relies entirely on a single Random House dictionary definition, ignoring more than one century of case-law on that issue. This is the linguistic equivalent of forum-shopping. You'll soon see why.

The sine qua non of a "wager" (as stated by numerous courts) is the "risk of loss" on both sides of the transaction. It's a contract where one side stands to win and the other to lose based on the outcome of the sporting event. DFS companies are indifferent to the result.

"In a wager or a bet, there must be two parties, and it is known, before the chance or uncertain event upon which it is laid or accomplished, who are the parties who must either lose or win."

Las Vegas Hacienda, Inc. v. Gibson, 77 Nev. 25, 29, 359 P.2d 85, 87 (1961)

Las Vegas Hacienda, Inc. v. Gibson, 77 Nev. 25, 29, 359 P.2d 85, 87 (1961)

See also:

Brown v. Bd. of Police Comm'rs of City of Los Angeles, 58 Cal. App. 2d 473, 477, 136 P.2d 617, 619 (1943)

Coors Brewing Co. v. Stroh, 86 Cal. App. 4th 768, 777, 103 Cal. Rptr. 2d 570, 577 (2001)

Alvord v. Smith, 63 Ind. 58, 62–63 (1878)

(same). Many more cases too.

Brown v. Bd. of Police Comm'rs of City of Los Angeles, 58 Cal. App. 2d 473, 477, 136 P.2d 617, 619 (1943)

Coors Brewing Co. v. Stroh, 86 Cal. App. 4th 768, 777, 103 Cal. Rptr. 2d 570, 577 (2001)

Alvord v. Smith, 63 Ind. 58, 62–63 (1878)

(same). Many more cases too.

See also Black's Law Dictionary:*

A wager is “a contract by which two or more parties agree that a certain sum of money or other thing shall be paid or delivered to one of them or that they shall gain or lose on the happening of an uncertain event."

*overlooked by IRS attorney

A wager is “a contract by which two or more parties agree that a certain sum of money or other thing shall be paid or delivered to one of them or that they shall gain or lose on the happening of an uncertain event."

*overlooked by IRS attorney

In the context of #DFS contests, the companies do not stand to win or lose anything based on the outcome of any particular sporting event. Thus, the entry fees should not be considered "wagers" under this well-settled definition. And there is case-law support for that. See below.

Here's one example (from Christie I):

"We note, however, the legal difference between paying fees to participate in fantasy leagues and single-game wagering as contemplated by the Sports Wagering Law."

NCAA v. Christie, 730 F.3d 208, 223 (3d Cir. 2013)

"We note, however, the legal difference between paying fees to participate in fantasy leagues and single-game wagering as contemplated by the Sports Wagering Law."

NCAA v. Christie, 730 F.3d 208, 223 (3d Cir. 2013)

"Entry fees for fantasy sports are not 'bets' or 'wagers' because (1) the entry fees are paid unconditionally; (2) the prizes offered to contestants are for amounts certain and are guaranteed to be awarded; and (3) Defendants do not compete for the prizes." See Humphrey v. Viacom

See Humphrey v. Viacom, Inc., Slip Copy, 2007 WL 1797648 (D.N.J.) (entry fees paid to participate in defendants' fantasy sports leagues are not “bets” or “wagers” because, inter alia, “[d]efendants do not compete for the prizes”)

See Las Vegas Hacienda v. Gibson, 77 Nev. 25, 359 P.2d 85 (1961) (offering prize to winner of competition does not constitute wagering contract if the offeror does not participate in the competition and has no chance of winning the prize).

The other key requirement is that the DFS operator must be "engaged in the business of accepting wagers." After all, that was the linchpin of the IRS memo's conclusion (see below):

To be deemed in the "business of accepting wagers," the company must "assume the risk of profit or loss" tied to the outcome of the sporting event. That's explicit in the Treasury Regs. Unlike bookmakers, DFS contest operators have no stake the outcome of the sporting event.

It's also expressed in the legislative history of the statute, as recognized by #SCOTUS:

"A person is considered to be in the business of accepting wagers if he is engaged as a principal who, in accepting wagers, does so on his own account."

US v. Calamaro, 354 U.S. 351 (1957)

"A person is considered to be in the business of accepting wagers if he is engaged as a principal who, in accepting wagers, does so on his own account."

US v. Calamaro, 354 U.S. 351 (1957)

"unambiguous legislative history showing that the excise tax applies only to one who is ‘engaged in the business of accepting wagers' as a ‘principal . . . on his own account.'

United States v. Calamaro, 354 U.S. 351, 360, 77 S. Ct. 1138, 1144, 1 L. Ed. 2d 1394 (1957)

United States v. Calamaro, 354 U.S. 351, 360, 77 S. Ct. 1138, 1144, 1 L. Ed. 2d 1394 (1957)

"A person is considered to be in the business of accepting wagers if he is engaged as a principal who, in accepting wagers, does so on his own account."

H.R.Rep.No.586, 82d Cong. 1st Sess. 56 (1951); Sen.Rep.No.781, 82d Cong. 1st Sess. 114 (1951),

H.R.Rep.No.586, 82d Cong. 1st Sess. 56 (1951); Sen.Rep.No.781, 82d Cong. 1st Sess. 114 (1951),

This language is clear and unambiguous. A person is considered to be engaged in the business of accepting wagers if he is engaged as a principal who accepts wagers “on his own account.”

Hayes & Conigliaro, 57 Drake L. Rev. 445, 455–56 (2009)

Hayes & Conigliaro, 57 Drake L. Rev. 445, 455–56 (2009)

A 1958 Senate Report offered the same interpretation: “A person is considered to be in the business of accepting wagers only (1) if he is engaged as a principal who, in accepting wagers, does so on his own account; or (2) if he assumes the risk of profit or loss." Id.

"This language also demonstrates Congress's view that a person is engaged in the business of accepting wagers for federal taxation purposes if the person has a stake in the wager." Id.

OK. Short break for dinner. Halftime.

The second half of this thread will continue shortly.

The second half of this thread will continue shortly.

The “risk of loss” on both sides of the transaction is essential to the finding of a “wager” and being “engaged in the business of wagering.” House-banked sports betting fits this paradigm, but DFS does not since contest operators are indifferent to result of the sporting event.

To be deemed in the "business of accepting wagers," the company must "assume the risk of profit or loss" tied to the outcome of the sporting event. That's explicit in the Treasury Regs. Unlike bookmakers, DFS contest operators have no stake the outcome of the sporting event

It's also expressed in the legislative history of the statute, as recognized by #SCOTUS:

"A person is considered to be in the business of accepting wagers if he is engaged as a principal who, in accepting wagers, does so on his own account."

US v. Calamaro, 354 U.S. 351 (1957)

"A person is considered to be in the business of accepting wagers if he is engaged as a principal who, in accepting wagers, does so on his own account."

US v. Calamaro, 354 U.S. 351 (1957)

"[The] unambiguous legislative history show[s] that the excise tax applies only to one who is ‘engaged in the business of accepting wagers' as a ‘principal . . . on his own account.'

United States v. Calamaro, 354 U.S. 351, 360, 77 S. Ct. 1138, 1144, 1 L. Ed. 2d 1394 (1957)

United States v. Calamaro, 354 U.S. 351, 360, 77 S. Ct. 1138, 1144, 1 L. Ed. 2d 1394 (1957)

“This language is clear and unambiguous. A person is considered to be engaged in the business of accepting wagers if he is engaged as a principal who accepts wagers “on his own account.”

Hayes & Conigliaro, 57 Drake L. Rev. 445, 455–56 (2009)

Hayes & Conigliaro, 57 Drake L. Rev. 445, 455–56 (2009)

“A 1958 Senate Report offered the same interpretation: “A person is considered to be in the business of accepting wagers only (1) if he is engaged as a principal who, in accepting wagers, does so on his own account; or (2) if he assumes the risk of profit or loss." Id.

"This language also demonstrates Congress's view that a person is engaged in the business of accepting wagers for federal taxation purposes if the person has a stake in the wager." Id.

In the context of #DFS contests, the companies do not stand to win or lose anything based on the outcome of any particular sporting event. Thus, the entry fees should not be considered "wagers" under this well-settled definition. And there is case-law support for that. See below.

Here's one example (from Christie I):

"We note, however, the legal difference between paying fees to participate in fantasy leagues and single-game wagering as contemplated by the Sports Wagering Law."

NCAA v. Christie, 730 F.3d 208, 223 (3d Cir. 2013)

"We note, however, the legal difference between paying fees to participate in fantasy leagues and single-game wagering as contemplated by the Sports Wagering Law."

NCAA v. Christie, 730 F.3d 208, 223 (3d Cir. 2013)

See Humphrey v. Viacom, Inc., Slip Copy, 2007 WL 1797648 (D.N.J.) (entry fees paid to participate in defendants' fantasy sports leagues are not “bets” or “wagers” because, inter alia, “[d]efendants do not compete for the prizes”)

See also Black's Law Dictionary:*

A wager is “a contract by which two or more parties agree that a certain sum of money or other thing shall be paid or delivered to one of them or that they shall gain or lose on the happening of an uncertain event."

*overlooked by IRS attorney

A wager is “a contract by which two or more parties agree that a certain sum of money or other thing shall be paid or delivered to one of them or that they shall gain or lose on the happening of an uncertain event."

*overlooked by IRS attorney

Coming up shortly:

- Explaining the distinction between “authorized” and “unauthorized” wagers for purposes of determining the proper tax rate. (Note: it does not mean “expressly authorized.”)

- Explaining the importance of the state-level “skill vs. chance” analysis

+ More

- Explaining the distinction between “authorized” and “unauthorized” wagers for purposes of determining the proper tax rate. (Note: it does not mean “expressly authorized.”)

- Explaining the importance of the state-level “skill vs. chance” analysis

+ More

The applicable tax rate hinges on whether it's an "authorized" or "unauthorized" wager under state law. For authorized wagers, the tax rate is 0.25%. For unauthorized wagers, the rate is 2%. But what do these words mean? Does authorized mean expressly permitted by statute? No.

The "authorized vs. unauthorized" dichotomy has been interpreted to mean "legal vs. illegal." The IRS has described it this way (see. e.g., FAQ #1 below), and so have cases and other legal authorities. This is an important distinction, for reasons that I'll explain shortly.

For example, daily fantasy sports is not expressly authorized by statute in California. But it's legal (and, hence, "authorized") because CA follows the "predominance" test for assessing skill vs. chance, and #DFS entails more skill than chance or luck. 25+ states use this test.

So, #DFS would be considered "authorized" under state law in every state (approx. 25-30) that employs the "predominance" test, regardless of whether such activity is expressly authorized by statute. And, in many states that use a lower threshold, DFS is authorized by statute.

In understanding why "authorized vs. unauthorized" really means "legal vs. illegal," also keep in mind that one reason for the higher tax rate (2%) is to curb illegal activity.

Here is case-law support:

"Under 26 U.S.C. § 4401, wagers illegal under state law are subject to a federal excise tax of two percent. Wagers not illegal under state law are subject to an excise tax of .25 percent."

Moser v. United States, 166 F.3d 1214 (6th Cir. 1998)

"Under 26 U.S.C. § 4401, wagers illegal under state law are subject to a federal excise tax of two percent. Wagers not illegal under state law are subject to an excise tax of .25 percent."

Moser v. United States, 166 F.3d 1214 (6th Cir. 1998)

It is incredibly misguided for anyone to suggest that the IRS counsel memo opens the door to potential criminal cases, especially when the memo expressly states that it "may not be used or cited as precedent" and that the question of legality was "not relevant" to the analysis.

I would also add that it's reckless and irresponsible -- especially in a publicly-traded environment -- to forecast the demise of the #DFS industry given the limited scope and non-binding nature of the IRS memo and the definitional flaws that I flagged earlier in this thread.

So, let's talk about the Wire Act. It's a non-starter because DFS operators are not in the "business of betting or wagering" (nearly identical language to the tax statute) since they do not assume a risk of profit or loss in connection with the outcome of a sporting event.

Consider this case as well:

"The test, of course, of whether one is engaged in wagering, is whether he is risking his money in a game of chance in which he may win, or lose, depending on the eventuality."

Rahke v. United States, 180 F. Supp. 576, 578 (Ct. Cl. 1960)

"The test, of course, of whether one is engaged in wagering, is whether he is risking his money in a game of chance in which he may win, or lose, depending on the eventuality."

Rahke v. United States, 180 F. Supp. 576, 578 (Ct. Cl. 1960)

The Court of Claims released that decision 1 year before Congress adopted the nearly identical "business of betting or wagering" language found in the Wire Act. Congress is presumed to have been aware of that decision interpreting the nearly identical language of the tax statute.

Those statutes, along with their legislative history and judicial interpretation, are strong evidence that when Congress referenced persons engaged in “the business of betting or wagering” in the Wire Act, it intended that language to refer to persons who wager on their own acct.

h/t and credit on the last tweet to:

Ben J. Hayes & Matthew J. Conigliaro, The Business of Betting or Wagering: A Unifying View of Federal Gaming Law, 57 Drake L. Rev. 445, 455–56 (2009)

Ben J. Hayes & Matthew J. Conigliaro, The Business of Betting or Wagering: A Unifying View of Federal Gaming Law, 57 Drake L. Rev. 445, 455–56 (2009)

Nor would the Illegal Gambling Business Act or Travel Act come into play, since those federal anti-gambling laws depend on a violation of state law, a topic beyond the scope of the IRS memo. And remember, the lack of statutory authorization does not mean illegal. See above.

Nor would the Illegal Gambling Business Act or Travel Act come into play, since those federal anti-gambling laws depend on a violation of state law, a topic beyond the scope of the IRS memo. And remember, the lack of statutory authorization does not mean illegal. See above.

It bears repeating:

"IRS internal memoranda are not binding on courts. Such informal, unpublished opinions of attorneys within the IRS are of no precedential value.”

Sierra Club Inc. v. Comm'r, 86 F.3d 1526, 1534 (9th Cir. 1996)

"IRS internal memoranda are not binding on courts. Such informal, unpublished opinions of attorneys within the IRS are of no precedential value.”

Sierra Club Inc. v. Comm'r, 86 F.3d 1526, 1534 (9th Cir. 1996)